High Down Payments And The Canadian Dream: An Affordable Housing Crisis

Table of Contents

The Soaring Cost of Housing in Canada

The escalating cost of housing in Canada is a significant barrier to homeownership. House prices have skyrocketed in recent years, particularly in major urban centers like Toronto and Vancouver, making it increasingly difficult for Canadians to afford a home.

- Average house prices in major cities: Toronto and Vancouver consistently rank among the most expensive cities globally, with average house prices well exceeding $1 million in many neighborhoods. Smaller cities are also experiencing significant price increases, albeit at a slower pace.

- Percentage increase in house prices over the past 5-10 years: House prices in many Canadian cities have seen double-digit percentage increases over the past decade, far outpacing wage growth. This rapid appreciation has dramatically reduced affordability.

- Comparison with income levels and affordability ratios: The ratio of house prices to average incomes has reached unsustainable levels in many areas, making homeownership unattainable for a significant portion of the population. Affordability ratios, which measure the proportion of income required for housing costs, are far higher than historical averages.

- Impact on different demographics: First-time homebuyers are disproportionately affected by high housing costs and high down payments. Families with children face additional challenges, as do lower-income earners and recent immigrants. The dream of homeownership is becoming increasingly elusive for many demographics.

The Impact of High Down Payments on Homeownership

High down payment requirements exacerbate the housing affordability crisis. The substantial upfront capital needed to secure a mortgage effectively excludes many potential homebuyers from the market.

- Percentage of income needed for a down payment in various cities: In expensive markets, securing a down payment can require saving a significant percentage of annual income, often exceeding 50% or even more for first-time buyers. This represents a major financial hurdle.

- Challenges faced by first-time homebuyers due to high down payments: First-time homebuyers often face the greatest challenges due to their lack of existing savings and limited access to financial resources. High down payments significantly delay their entry into the housing market.

- The effect of high down payments on saving timelines for aspiring homeowners: Saving for a significant down payment can take many years, even with diligent saving habits, potentially delaying major life milestones like family formation and financial security.

- The impact on family formation and generational wealth: The difficulty in affording a home is delaying marriage and family formation for many young Canadians, impacting the creation of generational wealth and further perpetuating inequality.

Factors Contributing to the High Down Payment Barrier

Several factors contribute to the high cost of housing and consequently, the high down payment barrier. Understanding these factors is crucial to developing effective solutions.

- Low housing inventory and high demand: A shortage of available housing units, coupled with strong demand, fuels price increases. This imbalance between supply and demand is a primary driver of high house prices.

- Speculation and investment in real estate: Investment in real estate, both domestic and foreign, contributes to rising prices, often pushing prices beyond what many average Canadians can afford. This speculative activity exacerbates the housing affordability issue.

- Rising interest rates and mortgage stress tests: Increasing interest rates and stricter mortgage stress tests further increase the financial burden on prospective homebuyers, impacting their ability to qualify for a mortgage.

- Government policies and regulations (e.g., foreign buyer taxes): While some policies aim to cool the market (like foreign buyer taxes), their effectiveness is often debated and their impact on affordability is complex.

- Limited affordable housing options: A persistent lack of affordable housing options, particularly social and rental housing, further compounds the problem, creating a cascading effect on the entire housing market.

Potential Solutions and Policy Recommendations

Addressing the high down payment barrier requires a multi-pronged approach involving both governmental and individual strategies.

- Increased housing supply through zoning reforms and infrastructure development: Easing zoning restrictions and investing in infrastructure can help increase the supply of housing units, potentially easing price pressures.

- Financial assistance programs for first-time homebuyers (grants, tax breaks): Government programs that provide financial assistance, such as grants or tax breaks, can help alleviate the burden of high down payments for first-time buyers.

- Addressing speculation and investment in the housing market: Policies that aim to curb speculation and investment in the housing market can help stabilize prices and make housing more affordable for average Canadians.

- Strengthening rent control measures to improve affordability for renters: Improving rental affordability through stronger rent control can also indirectly improve homeownership affordability by reducing the pressure on the housing market.

- Promoting sustainable and affordable housing construction techniques: Encouraging innovative and cost-effective construction techniques can contribute to building more affordable housing units.

Conclusion

High down payments present a significant obstacle to the Canadian dream of homeownership, impacting individuals, families, and the broader economy. The soaring cost of housing, combined with low inventory, speculation, and stricter lending requirements, has created an affordability crisis. Solutions must be multifaceted, focusing on increased housing supply, financial assistance for first-time homebuyers, and measures to curb speculation. The crisis of high down payments demands urgent action. Whether you're a first-time buyer facing daunting down payment requirements, a policymaker seeking solutions, or a concerned citizen, let's work together to find viable strategies to improve affordable housing and make the Canadian dream of homeownership a reality for all. Let's discuss solutions to tackle the issue of high down payments and create a more accessible housing market for all Canadians. Join the conversation and advocate for change around high down payments!

Featured Posts

-

Nottingham A And E Records Accessed Illegally Families Demand Justice

May 09, 2025

Nottingham A And E Records Accessed Illegally Families Demand Justice

May 09, 2025 -

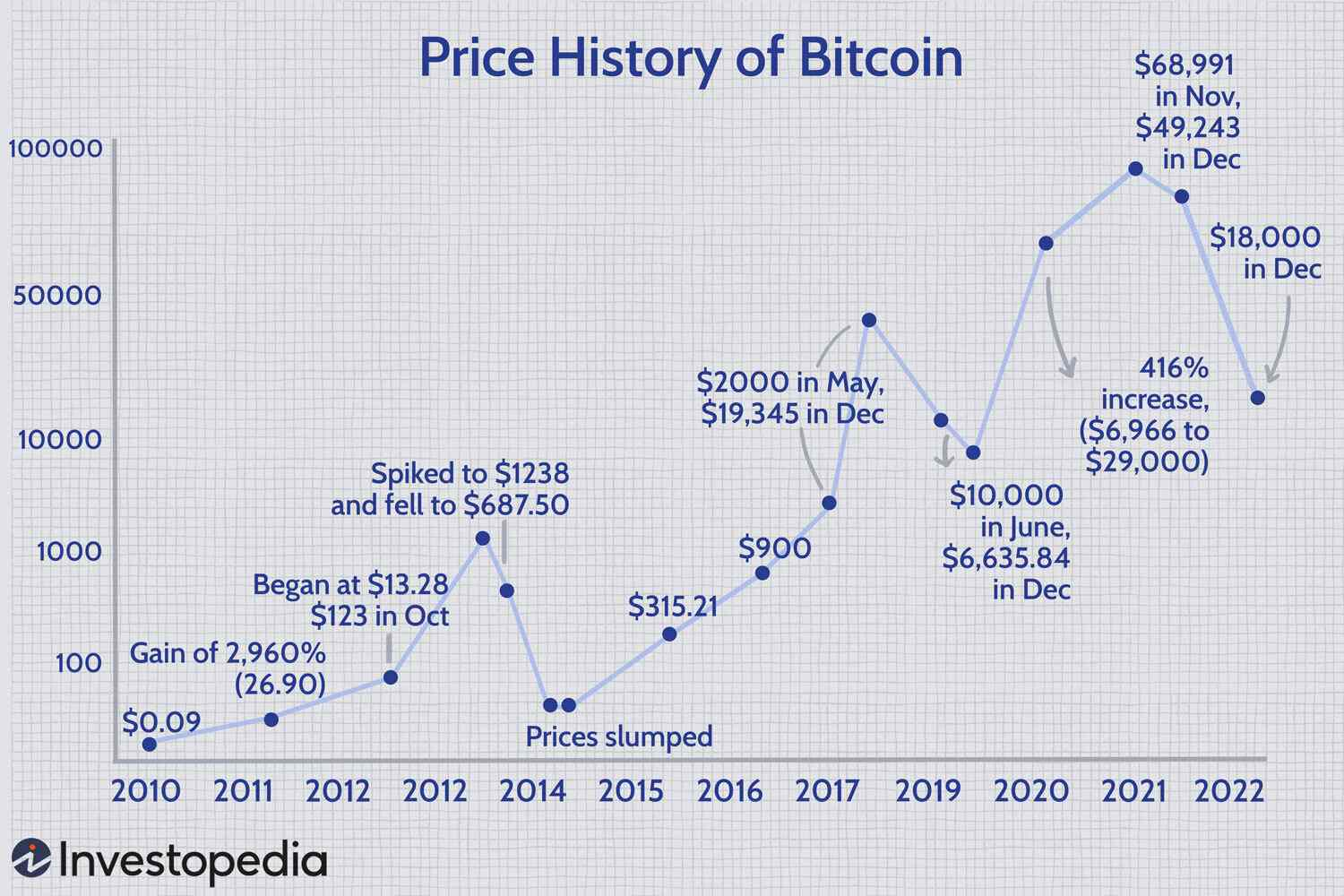

Bitcoin Price Prediction Evaluating The 100 000 Target After Trumps Speech

May 09, 2025

Bitcoin Price Prediction Evaluating The 100 000 Target After Trumps Speech

May 09, 2025 -

Ai Powered Design Figmas Challenge To Adobe Word Press And Canva

May 09, 2025

Ai Powered Design Figmas Challenge To Adobe Word Press And Canva

May 09, 2025 -

Black Rock Etf Poised For Massive Growth Billionaire Investment Insights

May 09, 2025

Black Rock Etf Poised For Massive Growth Billionaire Investment Insights

May 09, 2025 -

Major Funding Increase For Madeleine Mc Cann Case Investigation

May 09, 2025

Major Funding Increase For Madeleine Mc Cann Case Investigation

May 09, 2025